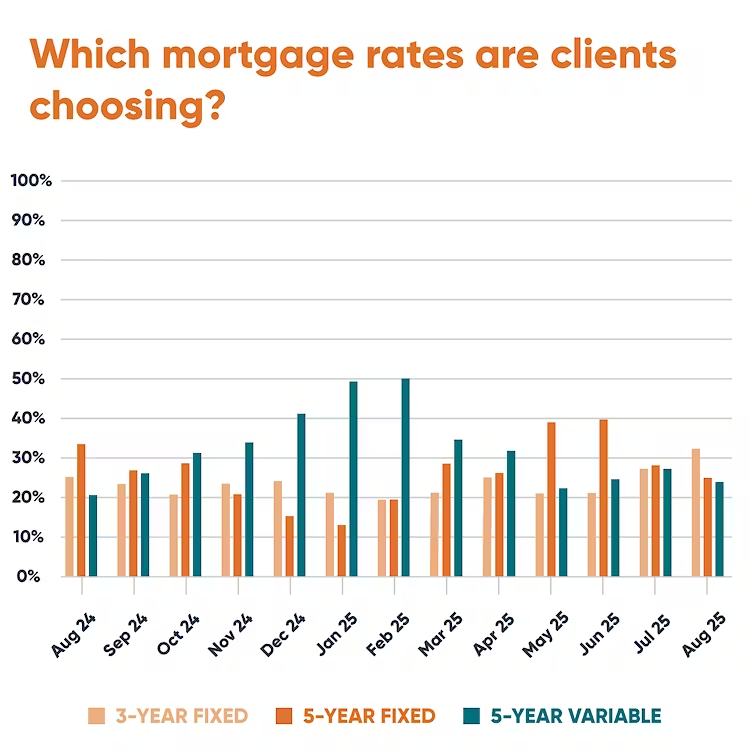

Choosing between a fixed-rate and variable-rate mortgage in 2026 is really about matching your financing to your risk tolerance, cash flow, and time horizon. Fixed rates offer payment stability and protection from future hikes, while variable rates provide flexibility and the potential for interest savings if conditions remain stable or improve.

Why This Decision Matters in 2026

In 2026, the Bank of Canada is expected to move away from aggressive rate cuts toward a more neutral stance, with many forecasts calling for policy rates to sit in roughly the mid‑2% range, plus or minus modest adjustments. For borrowers, this means that wild swings are less likely than in 2022–2024, but small changes can still impact qualification, stress testing, and long‑term affordability.

First‑time buyers and existing homeowners renewing their mortgages are especially affected, as even a 0.25% shift in rate can tighten or loosen their budget. Understanding how fixed and variable structures behave in this environment helps avoid surprises and supports better long‑term planning.

What a Fixed Rate Actually Means

A fixed‑rate mortgage locks in the interest rate for the entire term, most commonly 3 or 5 years, so your principal and interest payments remain the same every month. This predictability makes it easier to plan around other financial goals such as debt repayment, saving for retirement, or building an investment portfolio.

In 2026, most outlooks suggest 5‑year fixed rates will remain in a moderate range, influenced by government bond yields rather than directly by the overnight rate. For many households, this offers a “set it and forget it” option at a level that is neither ultra‑low nor crisis‑high.

Pros and Cons of Fixed Rates

Fixed rates shine for clients who value certainty above everything else. They offer:

- Stable payments, which simplify cash‑flow planning.

- Protection against potential future rate increases over the term.

The trade‑offs are:

- Fixed rates usually start slightly higher than comparable variable options.

- Breaking a fixed mortgage early can trigger large interest rate differential penalties, which can be costly if you sell, refinance, or restructure mid‑term.

For clients with long‑term plans in the same home and tight budgets, fixed often aligns best with broader financial planning.

What a Variable Rate Means in Today’s Market

A variable‑rate mortgage moves with the lender’s prime rate, which closely tracks the Bank of Canada’s policy rate. When the central bank adjusts its rate, lenders typically follow, and your mortgage rate responds accordingly—either through a change in payment or in the mix of interest versus principal.

In a 2026 environment where major hikes or cuts are less likely, variable rates can offer a relatively low starting point with the potential to benefit from any additional easing. However, there is still exposure if inflation re‑emerges or if global events force rates higher again.

Pros and Cons of Variable Rates

Variable rates tend to perform well over the long run when rates are stable or trending downward. They typically offer:

- Lower initial interest rates compared to fixed.

- More flexibility and often lower penalties if you need to break or refinance.

However, they also come with:

- Uncertain payments if rates rise, which can strain households with limited buffers.

- Emotional stress for clients who closely watch rate announcements and worry about changes.

Variable can be a good fit for clients with stronger cash flow, shorter time horizons, or a willingness to tolerate fluctuation in exchange for potential savings.

2026 Market Reality: When Each Option Makes Sense

Given current forecasts, 2026 looks more like a “normalizing” year than a crisis year for rates. In this context:

- Fixed mortgages may appeal to those who want to lock in a reasonable rate and avoid thinking about interest movements for the next several years.

- Variable mortgages may suit those who expect relative stability, are comfortable with risk, and might move or refinance within a 3–5 year window.

The narrowing spread between fixed and variable rates means the decision is less about chasing the lowest number and more about aligning with your broader financial strategy.

Timeline: How Long You Expect to Keep the Mortgage

Time horizon matters as much as the rate itself:

- 1–3 years:

Variable often performs better if rates stay flat or drift slightly lower, and it offers more flexibility if you sell or refinance. - 3–5 years:

Either option can work. Fixed is attractive if you are risk‑averse, while variable suits those who can handle some uncertainty and want potential savings. - 5+ years:

Fixed usually supports better long‑term planning, especially for households that do not want to manage payment changes year to year.

A Simple Cost Perspective

Consider a $500,000 mortgage amortized over 25 years. A 0.25% change in rate can translate into roughly $80–$120 per month in payment difference, or around $960–$1,440 over a year. While these numbers are approximations, they show how small movements in rates can either tighten or free up cash flow that could otherwise go toward investing, emergency savings, or other goals.

This is why the mortgage decision should not sit in isolation; it should be integrated into your broader financial plan.

How to Choose Based on Your Situation

From a financial planning perspective, the “right” mortgage structure depends on:

- Your cash‑flow flexibility and how much risk you can comfortably take.

- How long you realistically expect to keep the property or mortgage.

- Your other financial goals, such as paying down higher‑interest debt, investing, or building reserves.

For clients who prioritize stability, struggle with variability, or have long time horizons, fixed rates often align best. For those with stronger balance sheets, shorter expected terms, or a strategic view of rate cycles, variable can be part of a flexible, opportunity‑driven plan.

If you’d like, the next step can be to build a simple side‑by‑side scenario—fixed vs variable—using your actual numbers and integrating it with your overall financial plan.

💬 Reach out anytime:

📞 Call or text: 236-457-4230

📧 Email: rico@mypropertycentral.ca

🌐 Website: www.riccardomanazza.realtor

🏡 Explore more lifestyle stories: livingintheokanagan.ca

🤝 Team & listings: mypropertycentral.ca

📅 Book a meeting: Book A Call with Rico

Let’s Stay Connected

If you enjoyed this article or want to stay in touch with what’s happening in the South Okanagan real estate market, let’s connect online:

📸 Instagram: @riccardo_manazza_exp-realty

📘 Facebook: @riccardo.manazza.exp

💼 LinkedIn: Riccardo (Rico) Manazza

Follow for weekly market updates, behind-the-scenes insights, and tips from one of the Most dedicated REALTORS® in the Okanagan with eXp Realty and the My Property Central Real Estate Group.

For immediate assistance or to schedule a showing, contact my assistant (available 24/7) at 236-500-6778.

Disclaimer

This article is for informational purposes only and should not be considered financial or legal advice. Eligibility criteria and program details are subject to change. Always consult with a qualified mortgage professional and licensed REALTOR® for the most current information